A real estate bubble was created in Southern Utah as a direct result of pandemic induced home buying that was fueled by the Federal Reserve’s policies of pumping money into the economy and holding the Federal Funds Rate at zero.

How did we get here?

Banks were able to borrow money from the Fed for free, passing that money on to consumers in the form of 2% to 3.5% mortgage rates for most of the last two years. Record low mortgage rates, combined with the Covid pandemic, prompted droves of people to move out of large cities, resulting in home prices increasing at a near exponential rate.

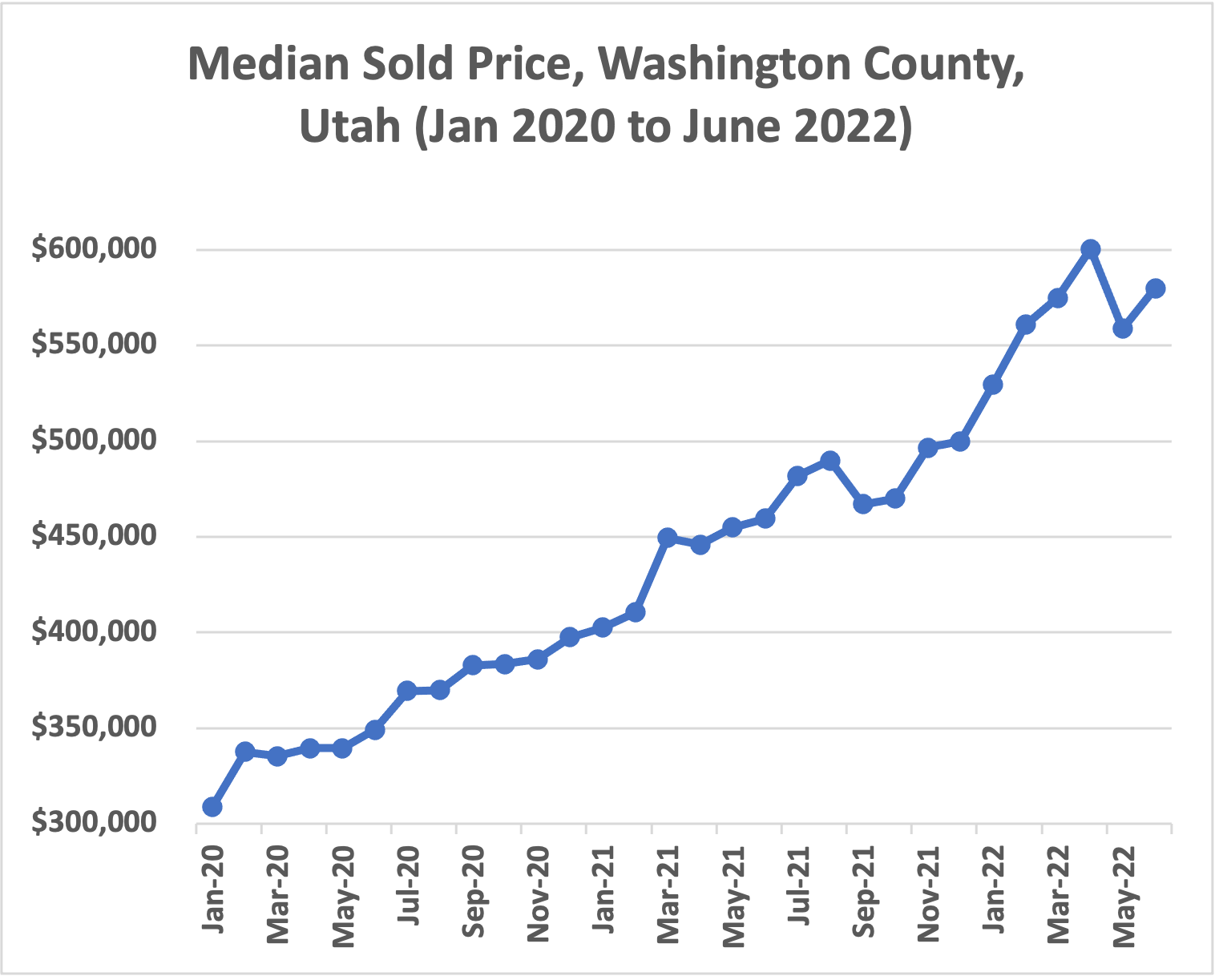

On January 1, 2020, two months before the pandemic began, the median sale price in Washington County, UT was $309,000. It accelerated to $470,000 in October 2021, and over the next 6 months shot up to $600,500 in April 2022. From pre-covid to this April, home values increased 94%!!!

At the beginning of this year, just 6 months ago, mortgage rates for a 30-year fixed rate loan were hanging out around 3.3% (MortgageNewsDaily.com). At the same time, inflation was 7.5% (Statista.com). Around that time, the Fed, taking inflation more seriously, began signaling that they were going to raise the federal funds rate. In anticipation of a rate hike, buyers scrambled to buy a home and lock in a low interest rate.

In my practice representing buyers and sellers, I witnessed irrational exuberance as many homebuyers frantically searched to find a home…any home. Already low levels of inventory combined with a mad dash to lock in a low interest rate created an environment where buyers settled. Forget about finding the perfect home, finding shelter for their families and locking in a low rate became imperative, coming at the cost of settling for a property that was less than ideal. Bidding wars were common on nearly every transaction, and the average house was selling for more than its asking price. It wasn’t sustainable.

Unfortunately, the Fed, believing that inflation was “transitory” (that’s Chairman Powell’s fancy word of choice) and a temporary shock due to global supply chain disruptions, waited too long to raise interest rates, only to shock the system with a 50 basis-point increase in May, and a 75-basis point increase in June (Federal Reserve), resulting in mortgage rates in excess of 6%, something not seen since 2008! Inflation is real and here to stay. Just look at the home values above or go fill up your gas tank if you want to see inflation first-hand.

With a global pandemic that will probably never end, a madman’s war in Ukraine, Americans being flush with cash from stimulus payments, and record low unemployment, there doesn’t seem to be any end in sight to this inflationary period.

It’s more expensive than ever to buy a house and get a loan

Today’s national average quote for a 30-year fixed rate loan is 5.65%, down from its peak of 6.28% seen on June 14, 2022. Remember, it was just 6 months ago that you could get a mortgage at 3.3%. When money was that cheap, buyers could swallow the higher prices of an inflated housing market. Now that mortgage rates are bouncing around in the fives and sixes, double what they have been, buyers can’t afford the combination of high home prices and high mortgage rates.

For example, if a person borrowed $400,000 on a 30-year fixed rate loan in January 2022, when rates were 3.29%, the monthly principal and interest payment would have been $1,749.62. Fast forward to today, at 5.65% interest, a person’s payment goes up $559.32 per month to $2,308.94. Home buyers should be outraged! In the last 6 months, it has become $560 more expensive per month to borrow the same $400,000, and the difference in interest paid over the life of the loan is over $200,000 more! Now we are talking about real money, and an adverse impact on a person’s wealth, which could impact families for generations.

Won’t some people be able to afford the more expensive mortgage payment? Sure. But most won’t. Most families are on a fixed income, and they can only afford a set amount each month. Think retirees who still carry a mortgage or the construction laborers who are building all the new houses around town. Going back to the example above, if a person can only afford a payment of $1,749.62, they could have borrowed $400,000 6 months ago. At today’s rates, that same payment only allows them to borrow $303,103.17. This person just lost nearly $100k in purchasing power! That person is now required to settle for a less expensive home (there are virtually no homes for sale in Washington County today for $300k) or is forced to abandon their home search until prices or mortgage rates fall. Factoring high rates and high prices together, it is 41% more expensive to buy a home today than it was in January, just 6-months ago!

What’s the market like today?

At the time of this writing, the supply of homes is nearly back to pre-covid levels; there are 985 homes listed for sale in Washington County on our local MLS. Back in February, there were about 400 homes on the market. Inventory has more than doubled in just a few months, as the rate of new listings hitting the market is up about 11% from this time last year, and the rate of sales is down almost 30% from this time last year! To view June’s market stats from the local MLS, click here. The impact of high prices and high interest rates is real, and the above data seems staggering, but we are only just now seeing the beginning of the bubble bursting. The most recent data we have for the County is from June. June’s closings were April and May’s pending sales. In April and May, house prices were going up, and buyers were irrationally exuberant about getting a house, any house. So, of course June’s data is going to seem a little rosy.

As your real estate broker, I promise to write to you again in early August to share the latest market stats with you. If mortgage rates remain high, I expect sales to be slower, inventory to be higher, and prices to be lower than today. In the coming weeks, I plan to write to you again, this time with strategies and ideas that I am implementing daily to get homes sold for top dollar in today’s new and falling market, ideas on how to get a lower mortgage payment, and ideas on how to sell now and avoid chasing the market down. If you are considering selling before my next message, please reach out to me; hit reply on this message or dial my cell number. It is (435) 773-3870.

I am Joe Allen, and I am ‘Southern Utah’s Home Adventure Guide.’ Buying or selling a home in any market can be a complex, challenging, and emotionally charged task. Let me take away some of the hassle and headache. Let me be your guide.

Sincerely,

Joe Allen

Joe Allen

‘Southern Utah’s Home Adventure Guide’

Principal Broker

Realty Absolute

P.S. Earlier this year my team and I celebrated a milestone and closed our 2,000th real estate sale! We would be honored and delighted if you would trust us to handle your next transaction.